Survive First, Grow Later: A Complete Risk-Management Blueprint for Forex, Gold & Commodity Traders

If there is one idea that defines Investment Trading Hub Academy (ITHA), it is this:

Professional traders obsess about risk first and returns second.

This first Education article is a deep, practical guide to building a risk framework you can actually use in forex, gold, and other liquid markets. It is not about “secret strategies” or magical indicators. It is about how you stay in the game long enough to let any edge you have actually work.

I will cover:

- Why risk management is non-negotiable (and what regulators are seeing in retail data).

- How to define risk in your own trading and investing.

- Position sizing, expectancy and risk of ruin in plain language.

- How leverage, margin and volatility interact in FX and gold.

- Psychological risk: loss aversion, revenge trading and overconfidence.

- A simple written risk plan you can adapt and use immediately.

- How all this ties into the structure of theitha.com.

Throughout the article I will suggest visuals you can create or embed to make the content more interactive for your readers.

1. Why Risk Management Is Non-Negotiable

Before we talk about techniques, it is worth facing the reality of retail trading.

1.1 What the numbers say

European and UK regulators have spent years analysing how retail traders actually perform, especially in leveraged products like contracts for difference (CFDs) and spread bets – the same tools many traders use for forex and gold.

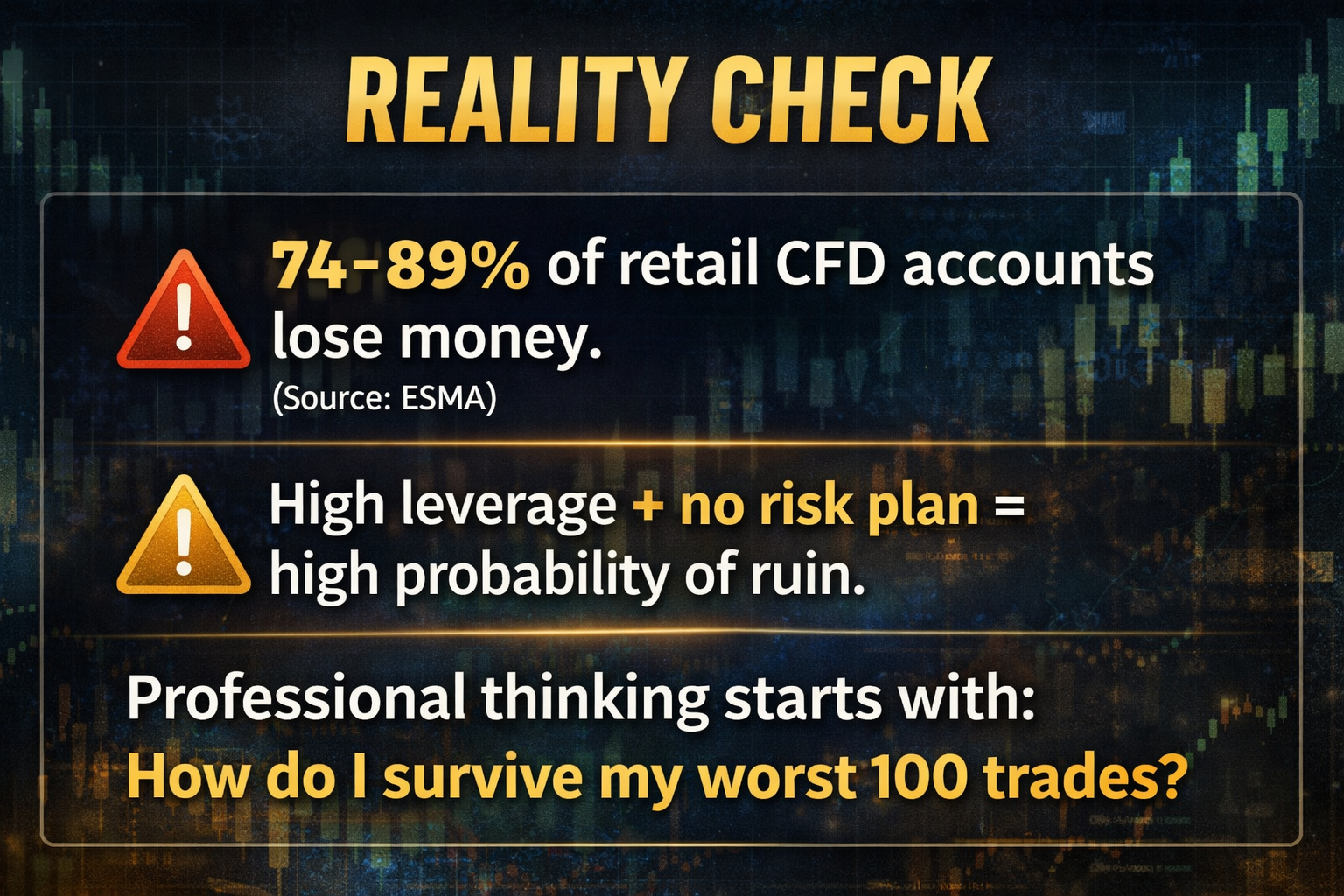

- The European Securities and Markets Authority (ESMA) found that 74–89% of retail CFD accounts lose money, with average losses per client between €1,600 and €29,000.

- Individual brokers, following EU and UK rules, now have to publish the percentage of retail accounts that lose money; many show loss rates around 70–80%.

At the same time, regulators are intensifying their crackdown on unregulated “finfluencers” who push high-risk trading without proper risk disclosure:

- The UK Financial Conduct Authority (FCA) has interviewed finfluencers under caution, issued dozens of alerts, and led international actions targeting illegal online financial promotions.

When you put those numbers together, you get a clear picture:

Most retail traders lose money – and a big part of the reason is poor or non-existent risk management, often combined with aggressive leverage and unrealistic expectations.

1.2 What this article is and is not

This article:

- Is general education on risk management concepts.

- Is not personalised investment advice or a guarantee of profits.

- Is not a recommendation to trade any specific instrument or to use leverage.

Any examples are there to illustrate principles. Your decisions must always take into account your personal situation, capital, jurisdiction and, ideally, the guidance of a qualified professional.

2. What “Risk” Actually Means in Trading & Investing

“Risk” is a word everyone uses but few define precisely. For the work we will do at ITHA, we will use a layered definition.

2.1 Market risk

This is the most obvious one: the chance that price moves against your position.

In FX, gold and commodities, this can be driven by:

- Economic data (inflation, jobs, GDP, central bank decisions).

- Geopolitics and macro shocks.

- Liquidity conditions (e.g., holiday sessions, after major news).

- Cross-asset flows (e.g., equities selling off, dollar strength, risk-off episodes).

Market risk is unavoidable. The only choice you have is how much exposure you take and how you define the point where your idea is invalidated.

2.2 Leverage and margin risk

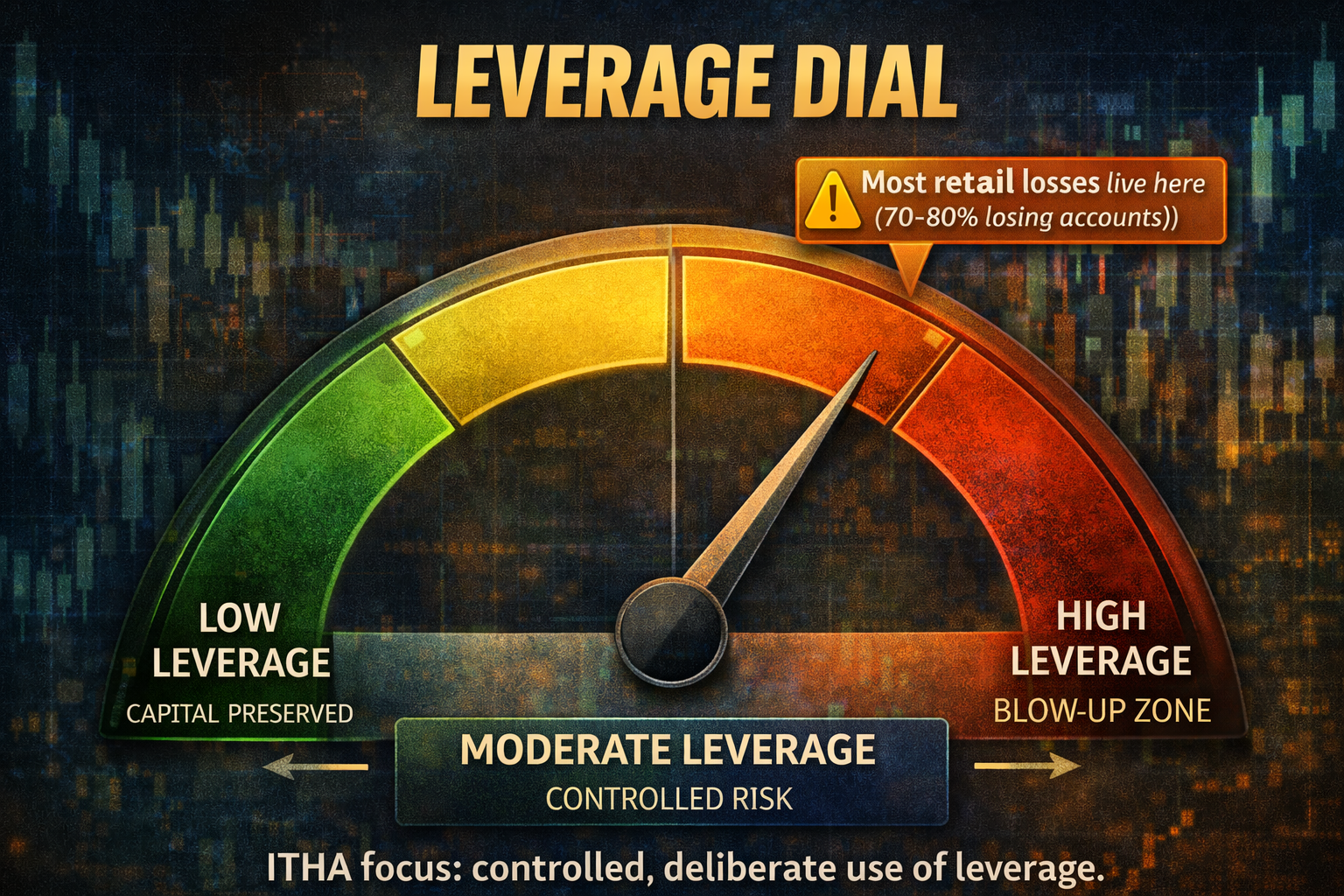

Leverage amplifies both gains and losses. A 1% move against you with 10:1 leverage is a 10% hit on your capital. With 30:1 it can wipe out a large chunk of your account very quickly.

This is why regulators repeatedly highlight that CFDs and other leveraged products are complex and high risk, and why so many retail traders lose money with them.

Leverage risk is not just about the size of losses, but about forced liquidation: if your margin is insufficient, positions can be closed by your broker at the worst possible time.

2.3 Liquidity and execution risk

Even on major FX pairs and gold, there are times when:

- Spreads widen.

- Orders slip or get filled at worse prices.

- Stops are triggered by short-lived spikes.

These are not bugs; they are part of how real markets work. Good risk management assumes that slippage and bad fills will happen from time to time.

2.4 Psychological risk

Perhaps the most underestimated layer is you.

Behavioural finance and prospect theory (Kahneman & Tversky) show that people feel losses about twice as strongly as equivalent gains – the famous “losses loom larger than gains” idea.

This loss aversion can lead to:

- Cutting winners too early to “lock in” small gains.

- Letting losers run because closing the trade would crystallise the loss.

- Revenge trading after a loss to “get it back”.

- Increasing size after a streak of winners out of overconfidence.

Understanding and managing your own psychology is a central part of risk management, not an optional add-on.

3. Designing Your Personal Risk Profile

Before you choose numbers (2% per trade, 5% monthly drawdown, etc.), you need to understand who you are as a trader or investor.

3.1 Key questions

Ask yourself:

- What is my true time horizon?

- Intraday… swing (days to weeks)… position trading… long-term investing?

- How stable is my income and cash flow?

- Is this a side project funded by savings, or capital you might need?

- How would I feel if I lost 20% of this account?

- Be brutally honest. If 20% would cause panic, your risk settings need to be more conservative.

- What is the main purpose of this account?

- Learning? Supplemental income? Long-term capital growth? Speculation?

Your risk profile is not fixed forever, but these questions define the starting constraints.

3.2 Separating accounts and objectives

One practical principle:

Do not mix rent money and experiment money in the same account.

Many traders benefit from having separate “buckets”:

- A learning / high-risk bucket with small capital, where you experiment deliberately with tight risk controls.

- A core capital bucket where risk per trade and monthly drawdown limits are much stricter and long-term sustainability is the goal.

This separation helps protect you from emotional spillover – and preserves your ability to keep trading after mistakes.

4. Position Sizing: The Steering Wheel of Risk

If there is one technique you must internalise, it is position sizing – how much you risk per trade.

Research by trading educator Van Tharp (building on earlier portfolio allocation studies) emphasises that position sizing can explain a huge portion of performance variability; in one often-cited study, “how much” accounted for around 90% of the variability in returns across portfolios.

Put simply:

Two traders with the same strategy can have completely different equity curves – purely because of how they size positions.

4.1 Defining risk per trade

A common way to define risk is:

Risk per trade (%) = (Account risk in money) ÷ (Account size)

For example:

- Account size: $10,000

- You decide to risk 1% per trade

- 1% of $10,000 = $100

That means: if your stop loss is hit, you lose $100 on the trade, regardless of how wide the stop is in pips or dollars.

To translate this into position size:

Position size = Dollar risk ÷ Stop size (in dollars per unit)

In FX terms:

- If your stop is 50 pips and each pip at 1 lot (100k units) is $10:

- 50 pips × $10 = $500 risk per lot

- You only want to risk $100:

- Position size = $100 ÷ $500 = 0.2 lots (20,000 units).

The same logic applies to gold, indices, etc.; you just map pip/tick value appropriately.

4.2 How much should you risk?

There is no universal magic number, but for most retail traders who want to survive:

- 0.25%–1% per trade is conservative and robust.

- 1%–2% is aggressive but still manageable with a proven strategy.

- Above 2% starts to become very stressful in real losing streaks.

The key is to pick a level that you can sustain psychologically during a run of losses, not just mathematically.

4.3 The impact of losing streaks

Losing streaks are normal, even with good strategies. What matters is how your account responds.

Example: Starting with $10,000

| Risk per trade | Loss after 5 losing trades | Loss after 10 losing trades |

|---|---|---|

| 0.5% | ≈ –2.5% (down to ~$9,750) | ≈ –5% (down to ~$9,500) |

| 1% | ≈ –5% (down to ~$9,500) | ≈ –10% (down to ~$9,000) |

| 2% | ≈ –10% (down to ~$9,000) | ≈ –18% (down to ~$8,200) |

| 5% | ≈ –23% (down to ~$7,700) | ≈ –40% (down to ~$6,000) |

At 5% risk per trade, ten losers can cut your account almost in half. Coming back from a 40% drawdown requires a 67% gain just to get back to breakeven – a brutally hard psychological and mathematical challenge.

At 0.5–1% risk per trade, you can experience normal losing runs and still stay in the game.

5. Expectancy and Risk of Ruin in Plain Language

Position sizing only makes sense when you combine it with expectancy – the average amount you can expect to win or lose per trade over the long run.

5.1 What is expectancy?

A simple formula for expectancy is:

Expectancy = (Win% × Average Win) – (Loss% × Average Loss)

Where:

- Win% is the probability of a winning trade (e.g., 45%).

- Average Win is the average profit in R (or dollars).

- Loss% is the probability of a loss (e.g., 55%).

- Average Loss is the average loss in R (or dollars).

Several trading education sources emphasise that without positive expectancy, no risk management will save you, and that aligning position size with expectancy is key to long-term survival.

Example:

- Win% = 40%

- Average win = +2.5R

- Loss% = 60%

- Average loss = –1R

Expectancy:

- (0.40 × 2.5R) – (0.60 × 1R) = 1.0R – 0.6R = +0.4R per trade

If your risk per trade is $100 (1R), then over many trades you might expect to make around $40 per trade on average, even though you lose more often than you win.

This is why a strategy can be profitable with a win rate under 50% if the average win is larger than the average loss.

5.2 Risk of ruin (conceptually)

Risk of ruin is the probability that your account will drop to a level where you can no longer trade (practically or emotionally).

Exact formulas can get technical, but the key drivers are:

- Risk per trade

- Expectancy

- Variance of results (how wild your R distribution is)

- Total starting capital

High risk per trade + low or negative expectancy = high risk of ruin.

Lower risk per trade + positive expectancy = very low risk of ruin, provided you stick to your plan.

For most retail traders, simply reducing risk per trade from 2–3% to 0.5–1% and removing reckless over-sized trades will dramatically reduce the risk of blowing up – even before their strategy is fully optimised.

6. Stops, Volatility and Practical Risk in FX & Gold

Good risk management does not just mean having a stop; it means placing it where the idea is invalid, not just where it “feels” safe.

6.1 Idea-based versus money-based stops

- Money-based stop: “I’ll risk $200, so I’ll put my stop 20 pips away because that fits the size I want.”

- Idea-based stop: “The trade thesis is invalid if price closes beyond this structure/level; I’ll calculate position size so that my risk at that stop equals my chosen % of capital.”

Idea-based stops are much more robust because they tie the risk to market structure, not arbitrary distances.

6.2 Using volatility measures

In FX and gold, volatility changes over time. A 30-pip stop might be extremely tight on some days and extremely wide on others.

Common ways to anchor stops to volatility include:

- Average True Range (ATR) – e.g., stop at 1–2× ATR beyond your entry structure.

- Recent swing highs/lows plus a volatility buffer.

- For gold (XAUUSD), combining key levels with ATR is particularly useful, as the instrument often has sharp intraday spikes.

The goal is to be far enough away to avoid normal noise, but close enough that if the market clearly proves you wrong, you are out with a pre-defined loss.

6.3 Beware of “guaranteed” stops

Some brokers offer guaranteed stop losses for a fee. Understand the terms:

- Are they only valid in normal conditions?

- Are there larger minimum distances?

- How does the additional cost affect your expectancy?

They can be useful, but they are not a substitute for a solid risk plan.

7. Leverage: Power Tool or Time Bomb?

Leverage is simply the ability to control a larger position with a smaller amount of capital. In regulated FX/CFD markets, you might see leverage such as 30:1 or more, especially for “professional” accounts.

Regulators keep repeating the same message: CFDs and similar leveraged products are very high risk, and a large majority of retail users lose money.

7.1 Why high leverage destroys accounts

With high leverage:

- Small price moves create large percentage swings in your equity.

- Normal volatility can trigger margin calls or forced liquidation.

- Emotional pressure increases, making discipline much harder.

Traders often overestimate their ability to handle leverage because they focus on the potential profit, not the probabledrawdown. When markets become volatile – for example, around major central bank announcements – even “tight” stops can be overrun.

7.2 Practical guidelines

Again, nothing here is personalised advice, but a few practical principles:

- Think in terms of percentage risk per trade, not maximum leverage available.

- Only use as much leverage as necessary to implement your position size based on your stop distance – not more.

- Be very cautious about raising leverage after a series of wins; this is when overconfidence peaks.

- Avoid holding highly leveraged positions through major high-impact events unless you fully understand gap risk and have factored it into your plan.

8. Psychological Risk: Managing the Person Behind the Screen

Even with a perfect mathematical risk plan, your results will collapse if you cannot execute it under pressure.

8.1 Loss aversion and the pain of being wrong

Prospect theory and decades of behavioural research show that people feel losses more intensely than gains of the same size.

Typical patterns:

- Taking small profits quickly to reduce the fear of them turning into losses.

- Refusing to close losing trades, hoping they will “come back”.

- Doubling down on losers to avoid “being wrong”.

Risk management must therefore include rules that protect you from your own brain.

8.2 Common emotional triggers

- Revenge trading

After a bad loss, you jump back into the market without a clear edge, often with bigger size, trying to “get your money back.” - Euphoria after a winning streak

You feel invincible, increase risk size, loosen criteria, and give back weeks or months of gains in a short burst of over-sized trades. - Fear of missing out (FOMO)

You enter late, take trades that do not fit your plan, or chase markets simply because they are moving. - Paralysis after a drawdown

You stop following your rules entirely, either by over-trading or under-trading, unable to pull the trigger on valid setups.

8.3 Practical psychological risk controls

- Pre-defined maximum daily loss

Example: “If I lose 2% in a day (or 3R), I stop trading for the day.”

This prevents tilt and revenge trading. - Weekly or monthly max drawdown

Example: “If I hit 6–8% drawdown on the account, I cut size by half and review my system before continuing.” - Mandatory cool-off rules

- After a big win or big loss: take a break, walk away from the screen for at least 30–60 minutes.

- No new trades opened immediately after closing a painful loss.

- Trading journal

Record not only entry, stop and target, but also:- Emotional state before and after the trade.

- Whether you followed your plan.

- Any rule violations.

Over weeks and months, your journal becomes the best diagnostic tool you have for psychological risk.

9. Building a Simple Written Risk Plan

Putting it all together, here is a template you can adapt.

9.1 Core parameters

- Account type and purpose

- Account name: “ITHA Trading Account – Learning / Core / Long-Term”

- Objective: e.g. “Compounding capital through high-quality FX & gold setups with strict risk controls.”

- Risk per trade

- Example: 0.5%–1.0% of account equity.

- Maximum daily / weekly loss

- Max daily: 2–3R or 1–2% of account.

- Max weekly: 4–6% of account (trigger a review if hit).

- Allowed instruments

- List the pairs and products you trade (e.g. EURUSD, GBPUSD, XAUUSD, US500, etc.).

- Avoid random “tourist trades” in unfamiliar markets.

- Timeframes and holding periods

- e.g. Intraday: M15–H1, no overnight holds unless explicitly planned.

- Swing: H4–D1, holding for several days if thesis remains valid.

- Stop-loss principles

- Stops are placed where the idea is invalid (structural levels + volatility buffer).

- All trades must have a pre-defined stop before entry.

- Position sizing method

- Always calculated based on % risk and stop distance (no guesswork).

- News and event rules

- Specify how you handle high-impact events (e.g. NFP, FOMC, CPI, central bank decisions).

9.2 Pre-trade checklist

Before every trade, run through a very short checklist (written and visible):

- Does this trade fit my plan and setup criteria?

- Is my stop in the correct location for the idea?

- Have I calculated the position size so that risk = X% of equity?

- Are there any major news events imminent that could interfere?

- Am I in a balanced emotional state, or am I trading out of boredom, FOMO or revenge?

If any answer is “no”, you do not take the trade.

10. Applying Risk Thinking to Long-Term Investment Ideas

ITHA is not only about short-term trading. It also includes long-term investment ideas – in FX, gold, commodities and broader markets.

The risk principles above still apply, with a few adjustments.

10.1 Position sizing in long-term ideas

For higher-timeframe positions:

- Stops are usually wider (in pips or dollars), but risk per trade in percentage terms should still be controlled.

- You might allocate, for example, 1–3% of your total portfolio to a single long-term thematic idea, depending on conviction and correlation.

10.2 Diversification and correlation

Diversification is not about owning many instruments; it is about owning exposures that do not all behave the same.

- Holding EURUSD, GBPUSD and AUDUSD long at the same time may look diversified, but much of the risk is actually USD-driven.

- Combining FX with gold or other commodities can add some diversification, but correlations can still increase dramatically during global stress.

Your risk plan should consider portfolio-level risk, not just single-trade risk.

10.3 Re-evaluation points

For long-term ideas, you may not want ultra-tight stops, but you still need clear points where the thesis is re-evaluated, for example:

- Breaks of key multi-month support/resistance zones.

- Major macro data or policy changes that invalidate the original story.

- Extended time decay (the idea simply not playing out after many months).

At each re-evaluation point you decide whether to:

- Hold with reduced size.

- Exit and look for a better opportunity.

- Scale up only if the thesis has been confirmed and your overall risk remains controlled.

11. How ITHA Will Help You Practise This Framework

The whole structure of Investment Trading Hub Academy at theitha.com is designed around this risk-first philosophy.

- Daily FX & Commodities

Regular breakdowns will not just say “price might go here or there”; they will emphasise context, key levels, and how a professional might think about risk around them. - Weekly Market Wrap

These pieces will connect the dots between macro events, sentiment, and positioning – so you can understand whythe market did what it did, not just what happened. - Investment Ideas

Longer-term themes will always include:- Clear scenarios (bull, bear, neutral).

- Key invalidation areas and approximate risk/reward profiles.

- Discussion of position sizing concepts for that type of idea (in general, not as personalised advice).

- Education (this category)

This first article is just the start. Upcoming pieces will dive deeper into:- Building and testing strategies.

- Trade journaling in a professional way.

- Advanced topics like regime filters, volatility targeting, and combining trading with long-term investing.

The goal is that, over time, you will have:

- A clear written risk plan tailored to your situation.

- The skills and concepts to adjust that plan as you grow.

- A structured hub (theitha.com) that supports you with daily, weekly and educational content aligned to that plan.

Comments ()