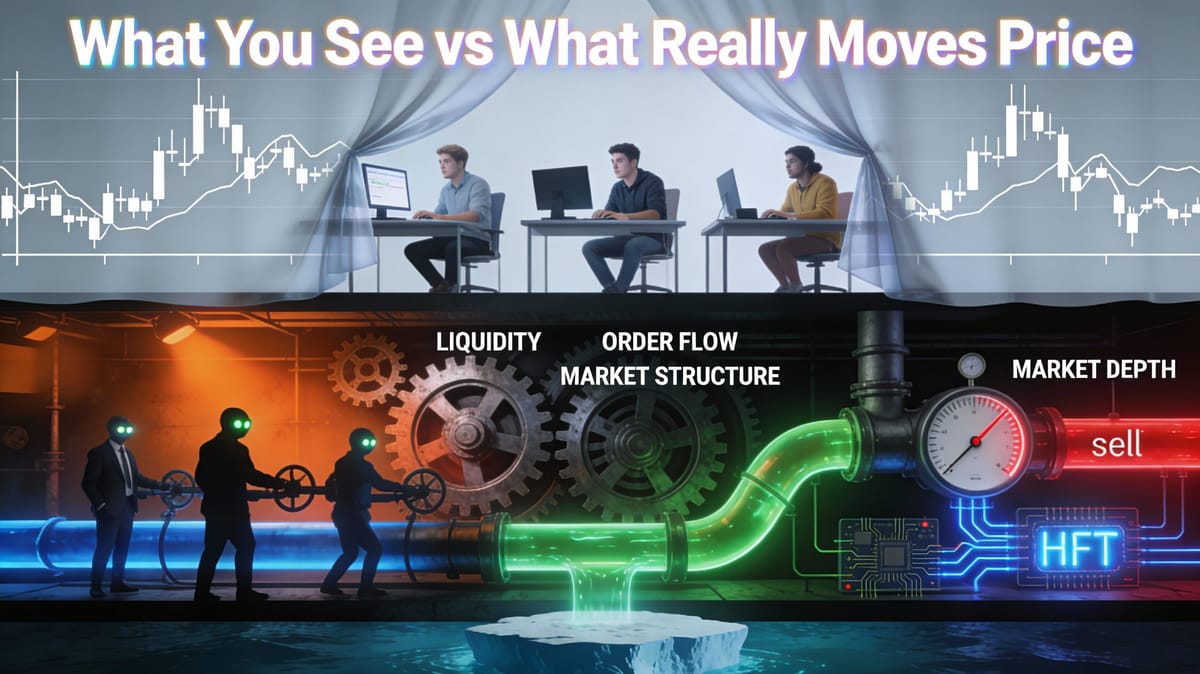

Liquidity, Order Flow, and Market Structure: The "Real" Engine of Price

Most traders spend their time analyzing patterns on candlestick charts, drawing trendlines, and watching indicators lag behind price action. But beneath every tick, every candle, and every sudden spike lies a deeper mechanism: the continuous interaction of liquidity, order flow, and market structure. Understanding this microstructural layer reveals how prices actually form, why they move the way they do, and what determines whether your trade idea is even executable at scale.

This is the engine room of markets—invisible to most, yet central to every transaction.

Understanding Market Microstructure: The Framework Behind Price

Market microstructure is the study of how trading mechanisms, rules, and protocols translate individual orders into observable prices and executed trades. It examines the detailed process by which buyers and sellers interact within specific institutional frameworks to discover price and exchange assets.

Equiti defines market microstructure as "the organisational and operational aspects of a financial market that facilitate trading," emphasizing its central role in price discovery and its importance for understanding liquidity and order flow dynamics. Zen Trading Strategies describes it as "the framework that governs how trades are executed" and stresses that grasping order flow and liquidity dynamics is critical to anticipating market movements and managing risk effectively.

Core components of microstructure

The microstructure of a market includes several interrelated dimensions:

- Trading venue and mechanism: Whether the market operates as a central limit order book (CLOB), a quote-driven dealer market, or a hybrid model with multiple venues and dark pools.

- Order matching rules: How buy and sell orders are paired—typically price-time priority in order-driven markets, but variations exist.

- Information transparency: What participants can observe—Level I (best bid/offer), Level II (full depth), or completely opaque (dark pools).

- Order types and execution protocols: Market orders, limit orders, stop orders, iceberg orders, and more exotic conditional types.

- Transaction costs and frictions: Bid-ask spreads, exchange fees, tick size constraints, and latency all affect who participates and how.

These structural features are not neutral; they shape who provides liquidity, how quickly information gets reflected in prices, and what execution quality looks like for different participant types.

Why microstructure matters for traders

For a practitioner, microstructure is not an academic curiosity—it determines:

- Whether a strategy that looks good on a chart can actually be executed profitably once you account for realistic costs and slippage.

- How much of your order will be visible to other participants, and how they might respond.

- What happens during stressed conditions when liquidity providers withdraw and the normal market structure temporarily breaks down.

Trading without understanding microstructure is like driving without knowing how the engine works: you can follow directions, but when something breaks, you're lost.

Liquidity: The Medium Through Which Orders Move Price

In finance, liquidity refers to the ease with which an asset can be bought or sold without causing significant price impact. It is not simply "volume"—a market can have high daily volume yet be fragile when you try to trade meaningful size quickly.

Dimensions of liquidity

Liquidity is multidimensional, encompassing several related but distinct concepts:

- Tightness: The bid-ask spread—the immediate cost of crossing from one side of the book to the other.

- Depth: The quantity of orders resting at or near the best bid and offer, indicating how much size can trade at the inside market without walking the book.

- Resiliency: How quickly the order book replenishes after a shock—whether from a large trade, news event, or technical disruption.

- Immediacy: The speed with which a trader can execute a desired quantity without delay or excessive market impact.

Zen Trading emphasizes that high-liquidity markets (such as major currency pairs) feature many active buyers and sellers, resulting in tight spreads and stable pricing, while low-liquidity markets exhibit wide spreads, sparse depth, and heightened volatility. Equiti highlights that narrow bid-ask spreads and deep order books indicate easier execution and lower trading costs, whereas wide spreads and shallow books signal higher friction and vulnerability to sudden moves.

Liquidity and price impact

Research on price impact demonstrates that when order book depth is shallow, even modest-sized market orders can move prices across multiple levels. Kukanov's work on order book events shows that both executed trades and changes to resting liquidity (additions, cancellations, modifications) influence the expected future price by altering the distribution of available liquidity at different levels.

This means liquidity is not just a convenience—it is a risk factor. Strategies calibrated during normal liquidity conditions can experience catastrophic slippage when liquidity evaporates during stress events, roll periods, or off-hours trading.

Liquidity regimes and crises

Markets transition between distinct liquidity regimes:

- Normal conditions: Spreads are tight, depth is ample, and the book refills quickly after trades. Small to medium orders execute with minimal impact.

- Stressed conditions: After shocks or during high uncertainty, liquidity providers widen spreads or withdraw orders entirely. The visible book thins dramatically, and aggressive orders produce exaggerated price moves.

- Crisis or illiquid regimes: In extreme cases (flash crashes, circuit breakers, off-hours), spreads widen to multiples of normal levels, depth vanishes, and price can gap violently.

Zen Trading notes that the 2010 Flash Crash illustrated how massive, one-sided order flow can overwhelm available liquidity, triggering rapid, temporary dislocations followed by partial recovery once liquidity returns. For traders, this underscores the importance of thinking in terms of liquidity risk, not just volatility risk.

Order Flow: The Force That Drives Price Discovery

If liquidity is the medium, order flow is the force acting upon it. Order flow refers to the continuous stream of buy and sell orders entering the market—their direction, size, aggressiveness, and timing.

Components and observables

Equiti breaks order flow analysis into several key components:

- Order book (limit order book): The collection of resting limit orders at various price levels, showing where passive liquidity sits and how deep the market is.

- Market orders: Aggressive orders demanding immediate execution by consuming resting liquidity, directly moving price by lifting offers or hitting bids.

- Limit orders: Passive orders that add liquidity to the book, defining potential support and resistance levels and shaping the depth profile.

- Bid-ask spread: The gap between the best bid and best ask, reflecting the immediate cost of demanding liquidity.

- Market depth: The total volume available at and beyond the inside quotes, indicating the resistance to price movement.

- Time and sales (tape): A chronological record of executed trades showing price, size, and timestamp, revealing the pace and character of actual transactions.

Zen Trading describes order flow as a "real-time report card" of market activity, noting that large waves of buy or sell orders can shift prices rapidly, while a lack of interest can signal uncertainty or impending volatility.

Order flow and price formation

Order flow is central to price discovery because it reveals real-time imbalances between supply and demand:

- A surge of aggressive buy orders exhausting offers at successive levels pushes the best ask higher and raises the prevailing trading price.

- Persistent sell-side aggression hitting bids drives price lower and often widens the spread in weaker market conditions.

- Large clusters of passive orders ("walls" of bids or offers) can temporarily halt price movement until those orders are either consumed or pulled.

Equiti emphasizes that analyzing order flow allows traders to reveal supply and demand zones, identify support and resistance, gauge market sentiment in real time, and forecast potential price swings before they fully materialize. Zen Trading adds that unusual order flow events—such as those seen during flash crashes—typically reflect massive, one-sided flows overwhelming available liquidity.

Order flow imbalance and directional pressure

Specialized research on order flow imbalance (the net difference between buy-initiated and sell-initiated volume over a period) shows strong correlations with short-term price pressure. When buy imbalances dominate, price tends to rise as liquidity at the offer is progressively consumed; when sell imbalances dominate, the opposite occurs. For intraday traders, monitoring order flow imbalance can be more informative than lagging technical indicators because it directly captures who is in control at the margin.

Market Structure: The Rules That Shape the Game

Market structure defines the institutional and technological framework within which liquidity and order flow interact. It determines how orders are matched, what information is visible, who can participate, and what execution quality different traders experience.

Order-driven vs dealer markets

Classical microstructure distinguishes between:

- Order-driven markets: Central limit order book systems (most modern equity and futures exchanges) where prices emerge from the aggregation of many participants' limit orders, and the book itself is the primary mechanism of price formation.

- Dealer or quote-driven markets: Markets where designated dealers or market makers quote bid and ask prices and internalize order flow, managing inventory risk (common in OTC FX and some fixed income markets).

- Hybrid and fragmented markets: Environments with multiple venues (lit exchanges, dark pools, internalizers) where routing logic and venue selection materially affect execution outcomes.

These structural differences affect transparency, queue priority, access to hidden liquidity, and the speed required to compete effectively.

Order types and hidden liquidity

Modern trading venues support a wide array of order types beyond simple market and limit orders:

- Stop and stop-limit orders: Conditional orders triggered when price trades at a specified level, commonly used for risk management but also contributing to cascading moves when stops cluster.

- Iceberg (reserve) orders: Orders that display only a small portion of their true size; as the visible slice is filled, another portion becomes visible. Zerodha explains that iceberg orders are designed to break large orders into smaller disclosed "slices" to hide full size and reduce market impact, making them valuable for institutions wanting to minimize signaling.

- Hidden, pegged, and midpoint orders: Orders that do not appear on the visible order book or that adjust their price dynamically relative to the inside market.

Optiver's explainer on order books illustrates how matching engines prioritize orders by price and then time, building a queue of resting orders at each level from many participants. The presence of hidden and iceberg orders means the visible book is only an approximation of true liquidity—the real capacity at each level can be significantly larger and adaptive.

This opacity creates asymmetry: sophisticated participants can detect hidden liquidity through statistical patterns or direct information, while retail traders see only the superficial layer.

Dark pools and off-exchange liquidity

Dark pools are private trading venues that allow institutional investors to execute large orders without revealing their intentions to the public market. TradersPost notes that dark pools account for approximately 15-20% of total U.S. equity trading volume, making their liquidity patterns essential knowledge for serious traders.

Dark pools operate as alternative trading systems (ATS) that match buyers and sellers without displaying order information publicly until after execution. The primary advantage is preventing market impact: when institutions need to trade large quantities, executing on public exchanges would typically move prices against them, whereas dark pools provide liquidity without pre-trade transparency.

However, this comes at a cost: price discovery occurs on lit venues, and dark pool participants may receive worse fills if their order interacts with stale quotes or informed flow. For retail traders, detecting dark pool activity (via unusual volume spikes, post-execution prints, or discrepancies between visible depth and actual trades) can provide insight into institutional positioning.

High-Frequency Trading and Market Making: The Modern Liquidity Providers

The rise of high-frequency trading (HFT) has fundamentally reshaped market microstructure, with algorithmic participants now dominating liquidity provision in many venues.

HFT as market makers

Academic research shows that HFTs have become the de facto market makers in modern electronic markets, replacing traditional low-frequency market makers. Using data from NYSE Euronext Paris with specific identifiers for electronic market-making activity, studies find that HFTs do provide liquidity to the market, but strategically—they avoid being adversely selected by other fast traders by conditioning their quotes on observed flow with near-zero latency.

Theoretical models of HFT market making reveal several important dynamics:

- HFTs can cancel limit orders extremely quickly after receiving adverse signals, creating a winner's curse for slower market makers who cannot react as fast.

- This speed advantage causes low-frequency market makers to widen spreads or reduce depth, potentially deteriorating overall market liquidity unless HFTs fully replace traditional liquidity providers.

- HFT liquidity provision is U-shaped as a function of volatility: it first increases as volatility attracts more trading opportunities, but then decreases sharply when price volatility exceeds a threshold, precisely when liquidity is most needed.

This fragility has policy implications: markets can become unstable during stress when HFTs withdraw, leaving few participants willing to provide liquidity. Research also suggests that policies like minimum resting times or cancellation taxes may improve liquidity in low-volatility environments but further reduce it during high volatility, when it would be most valuable.

Order flow segmentation by speed

Research on order flow segmentation and latency delays demonstrates that order flow is effectively divided by participant speed. Fast traders observe the flow of slower participants and can condition their responses with minimal delay, extracting value from information asymmetry. This segmentation means different trader types face different effective markets, even when nominally trading on the same venue.

For retail and institutional traders without sub-millisecond latency, this implies that displayed liquidity may evaporate just as they attempt to access it, and that strategies assuming stable, observable depth may underperform in practice.

Algorithmic Execution: VWAP, TWAP, and Smart Order Routing

Institutional traders rarely execute large orders with a single market order; instead, they use algorithmic execution strategies designed to minimize market impact and achieve benchmark performance.

VWAP algorithms

Volume Weighted Average Price (VWAP) algorithms aim to execute trades in proportion to the market's historical or predicted volume profile, so that the average execution price approximates the day's VWAP.

VWAP divides the total order into smaller tranches and submits each proportionally to observed or predicted market volume, masking the order and reducing market impact. Financial Edge Training explains that VWAP is calculated by summing the product of price and volume for each trade, then dividing by total volume, providing a benchmark for assessing execution quality.

VWAP is most effective when:

- The order size is large but not overwhelming relative to daily volume.

- Intraday volume patterns are predictable.

- The goal is discretion and completion within a single session.

However, VWAP has limitations: if the realized volume distribution differs significantly from the historical profile (e.g., an unexpected news event shifts volume patterns), the algorithm's average price may deviate substantially from the benchmark, leading to either outperformance or underperformance by chance. Additionally, VWAP does not adapt to sudden liquidity changes or aggressive competing flow.

TWAP and POV algorithms

Time Weighted Average Price (TWAP) algorithms split orders evenly over time, regardless of volume patterns, and are suitable when volume is unpredictable or when the trader wants consistent pacing. Percentage of Volume (POV) algorithms participate at a fixed percentage of market volume, adapting to changing liquidity conditions but risking slow completion if volume drops.

The choice among VWAP, TWAP, and POV depends on market conditions (liquidity, volatility, urgency), order characteristics (size, time horizon), and the benchmark used to evaluate performance (arrival price vs VWAP vs implementation shortfall).

Smart order routing and execution quality

In fragmented markets, smart order routing algorithms scan multiple venues (exchanges, dark pools, ECNs) to find the best available price and hidden liquidity. Institutions use these tools to minimize information leakage and reduce transaction costs, but the complexity of modern market structure means execution quality varies significantly across brokers and algorithms.

For retail traders, understanding that large orders are executed algorithmically and often via dark pools helps explain why price action sometimes diverges from visible order book changes—significant institutional activity may be occurring off-screen.

How Liquidity, Order Flow, and Structure Jointly Determine Price

Price is not an abstract output of "supply and demand"; it is the concrete result of specific orders interacting with the order book under precise structural rules.

Mechanics of price impact

Empirical studies document several consistent patterns in how orders move price:

- Market orders that consume liquidity at the best price shift the mid-price by an amount proportional to trade size and inversely proportional to local depth.

- Limit order additions and cancellations also affect the expected future price by changing the distribution of potential trades at different levels, even if no transaction occurs.

- Impact is concave: Doubling trade size increases impact less than twofold, but repeated trades in the same direction produce cumulative effects that can become semi-permanent.

Duong's thesis on limit order book events and price formation shows that different types of order book events (submissions, cancellations, executions) contribute differently to transient versus persistent components of price, with aggressive trades having larger immediate impact and passive order flow shaping longer-term price levels.

Reading the tape: combining flow and book structure

Practitioners who combine time-and-sales data (the "tape") with Level II order book snapshots can infer:

- Directional pressure: Are trades predominantly hitting the bid (bearish flow) or lifting the offer (bullish flow)?

- Liquidity dynamics: Are large resting orders being consumed, or are they being pulled before impact? Is depth refilling or thinning?

- Hidden participants: Are trades executing at sizes far exceeding visible depth, suggesting iceberg or dark pool activity?

Equiti emphasizes that this real-time analysis helps reveal supply and demand zones, identify support and resistance levels, gauge sentiment, and forecast price swings before they fully develop. Zen Trading adds that traders who fail to account for rapidly changing liquidity dynamics risk getting trapped in illiquid positions or misinterpreting normal microstructural noise as meaningful trend shifts.

Practical Implications: Trading With the Engine, Not Against It

Understanding market microstructure should fundamentally change how you approach trade planning, execution, and risk management.

Adapt strategy to liquidity and structure

Different strategies require different liquidity environments:

- Scalping and high-frequency approaches require stable, deep books and low latency; they fail when spreads widen or when trade size is large relative to top-of-book depth.

- Swing and position trading is less sensitive to tick-level microstructure but still depends on the ability to enter and exit without prohibitive slippage, especially during stressed conditions.

- Event-driven strategies must plan for liquidity evaporation and sudden jumps—stop orders may not fill at expected levels, spreads can widen dramatically, and market orders may suffer extreme impact.

Position sizing and liquidity risk

Traditional risk management relying solely on volatility (e.g., ATR stops, fixed percentage risk) is incomplete without considering liquidity:

- Gap and slip risk: In thin books, stop-loss orders are triggers, not guarantees of exit at the specified price.

- Capacity constraints: At some size, your own orders materially affect order flow and price, degrading the edge that was estimated at smaller scale.

- Correlated liquidity events: During crises, liquidity deteriorates across multiple assets simultaneously; portfolio risk models assuming independent, stable liquidity underestimate true drawdown potential.

Institutional research emphasizes the need for liquidity-adjusted risk models and execution cost estimates that go beyond simple volatility-based measures.

Monitoring microstructural health

Ongoing market monitoring should include microstructural indicators:

- Spread dynamics: Widening spreads often precede volatility spikes or trend exhaustion.

- Depth changes: Sudden withdrawal of resting orders or asymmetric depth (deep bids vs shallow offers, or vice versa) signals directional pressure.

- Order flow character: Shift from passive liquidity provision to aggressive taking indicates rising conviction or urgency.

Zen Trading suggests that as technology and algorithmic participation continue to advance, traders who integrate order flow and liquidity analysis will maintain a persistent edge over those relying solely on higher-timeframe price patterns.

Conclusion: Seeing Through the Surface

Liquidity, order flow, and market structure are the true engine of price—the mechanism that turns individual decisions into the ticks, candles, and trends displayed on your chart. Mastering this layer means:

- Seeing price not as an independent series but as the outcome of specific orders interacting in a structured environment.

- Recognizing liquidity as a distinct risk factor with regimes that can shift faster than volatility alone predicts.

- Using order flow to gauge who controls the margin and when imbalances are building that will force price adjustment.

- Understanding structure—venues, order types, HFT participation, dark pools—so you know what execution quality is realistic and how to position accordingly.

For serious traders, this perspective shifts focus from "predicting price" to reading the machine: the constantly updating limit order book, the flow of aggressive and passive orders, and the structural rules governing their interaction. It is this understanding—more than any indicator or pattern—that separates those trading with the engine from those being ground by it.

Comments ()